Social protection schemes look very different across the world. They traditionally protect people from income fall after shocks. But some programmes have higher aims: increasing the economic opportunities and promoting the potential of those who are socially excluded.

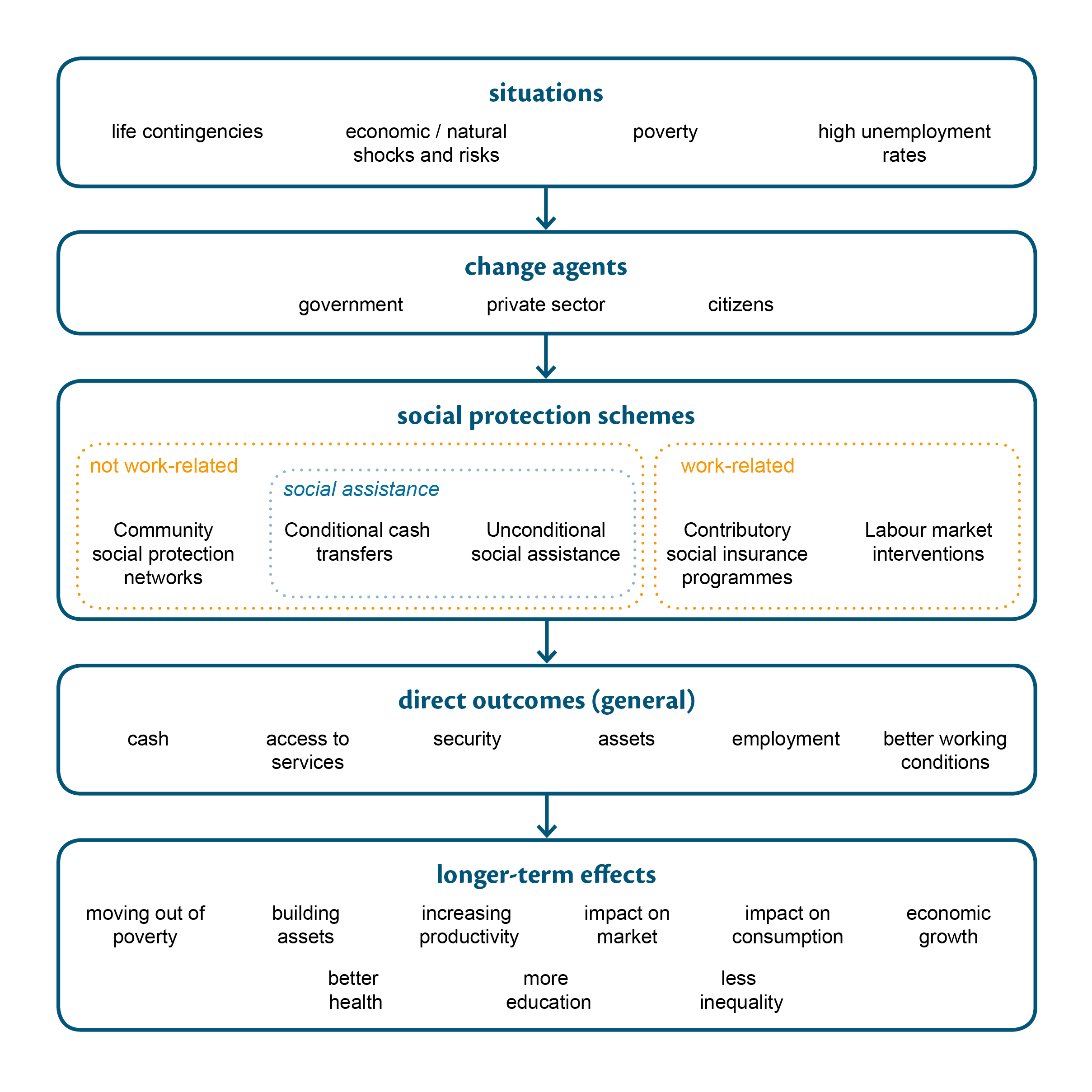

Social protection is a broad concept embracing protective and sometimes promotive measures that are needed in different situations and targeted at different groups and under different conditions. On the basis of these distinctions, this article divides social protection into four categories: conditional cash transfers, unconditional social assistance, contributory social insurance programmes, and labour market interventions.1

All of these categories are first of all protective: they aim to protect citizens against a severe fall in income as a result of economic, natural or life shocks and to improve access to social services. In developing countries, however, conditional cash transfer programmes and labour market interventions in particular aim more directly to increase development and economic opportunities and are therefore more promotive. All social protection programmes are targeted at those who need it most. For a discussion on targeted versus universal social protection, see ‘Social protection as a global challenge’.

Setting up social protection programmes involves a number of agents: governments, the private sector and civil society. These programmes can have different short and longer-term economic and development-related effects. The process from the need for social protection schemes, to their setting up and their outcomes is shown in figure 1, from the perspective of the (potential) receiver. This article will address these elements for each category of social protection.

Like the other articles in The Broker’s Social Protection Dossier, this article focuses mainly on developing countries. The categorization it proposes, however, applies to both developing and developed countries. As will be shown later, some types of social protection programmes, such as conditional cash transfers, are more widespread in developing countries than others, such as contributory social insurance schemes.

Conditional cash transfers

The purpose of the first category of social protection programmes, conditional cash transfers, is often both protective and promotive. They protect people against poverty and help them increase their economic opportunities and raise their standards of living. These programmes are part of what is often called ‘social assistance’ and are implemented mainly in middle income countries. Latin America has the most experience with these programmes, while only a limited number of programmes have been established in Africa. Table 1 lists some 50 conditional cash transfer programmes in developing countries.

Poor and vulnerable people targeted by a conditional cash transfer programme receive money only if they meet the attached conditions, such as the recipient or their children regularly attending school or visiting a medical centre.3 The programmes sometimes also offer training in a diverse range of skills, such as financial management, and try to improve the recipients’ self-confidence.

According to Stephen Devereux and Melese Getu, one reason for attaching conditions to transfers is ‘that social protection can be more effective and sustainable in the long run if it is linked to investment in human capital formation’.4 These programmes therefore do more than just provide the poor with extra money. Governments argue that if the programmes encourage children to go to school more regularly and help them and their parents to improve their health by visiting health centres more frequently, they can have a sustainable effect on wellbeing and on the economic opportunities of the beneficiaries, as well as of future generations.

Some recent conditional cash transfer programmes also explicitly target workers in the informal economy, farmers, and other self-employed people. This is important, says Hans-Horst Konkolewsky, Secretary General of the International Social Security Association, especially now that the informal sector seems to be expanding.5 These people are usually excluded from work-related protection mechanisms like social insurance and labour market interventions. In 2009, the Argentinian conditional cash transfer programme Asignación Universal por Hijo expanded its scope to include the families of informal workers and of unemployed persons. The Indonesian Program Keluarga Harapan is targeted at maternal and neonatal health for mothers working in the informal sector. The number of programmes that reach informal workers, however, remains limited.

Table 1 Conditional cash transfer programmes

| Latin America | |||||||

| Argentina |

|

||||||

| Belize |

|

||||||

| Bolivia |

|

Many evaluation studies find that conditional cash transfer programmes like Oportunidades in Mexico and Bolsa Família in Brazil have a positive effect on poverty reduction and on the educational level and health of the beneficiaries.6 World Bank experts Bénédicte de la Brière and Laura B. Rawlings write that the poorest and most vulnerable groups are better protected against shocks.7 Nevertheless, the studies also show that differences between programme participants and non-participants remain limited, and that the increase in income and educational level among the participants is small.

Cash transfers are often granted to women, but whether this contributes to their empowerment is debatable. Although they may gain in economic terms, women are also frequently responsible for making sure the conditions are met. It is they who most often send their children to school, visit medical centres or attend talks on health. Granting the cash to women may therefore increase the time they have to spend on household activities at the expense of paid employment. In some cases, as Maxine Molyneux writes, their greater autonomy has also led to more violence towards them from male family members.8

Social protection consultant Nicholas Freeland is critical of conditional cash transfers. There may be evidence for improvements in health and education level, ‘but who is to say whether this is a feature of the “conditionality” rather than of the transfer itself (or simply the fact of a predictable source of regular income)?’.9 Freeland adds that there is evidence to show that cash transfers without conditions lead to similar improvements. Other studies show that the effects of conditional cash transfer programmes on reducing child labour are ambiguous. Some evaluations observe a decrease in child work, but others find no evidence to support this conclusion.

The implementation and maintenance costs of conditional cash transfer programmes are high and their administration is time-consuming, as GSDRC writes.10 Moreover, they can operate effectively only if public services are of sufficient quality and are well distributed across the country.

The promotive aspect of conditional cash transfers allows the poorest and most vulnerable people to improve their skills and health and therefore their chances on the labour market. This can help them escape poverty permanently. Researchers do not agree, however, on whether conditionality is the best way to pursue promotive objectives.

Unconditional social assistance

Unconditional social assistance programmes first and foremost serve a protective purpose. They provide income security, often through cash transfers, to people who are faced with contingencies and consequently suffer a temporary or permanent loss of income. Assistance can consist of social pensions, disability benefits, survivors benefits and family or child benefits. Unemployment benefits that are not paid through an employer can also be considered a form of unconditional social assistance. Eligibility does not depend on work history, only on being unemployed. Tables 2 and 3 provide an overview of unconditional social assistance programmes in developing countries.

As unconditional social assistance programmes and conditional cash transfer programmes share the aim of protecting people against poverty and improving health and wellbeing among certain groups, some institutions and researchers do not make a distinction between the two. However, this article retains the distinction because unconditional social assistance programmes do not in the first instance aim at longer-term development or a permanent move out of poverty; their primary purpose is income redistribution and income security in times of shocks.11

The name says it all: unconditional social assistance programmes do not attach conditions to receiving the benefits. Recipients must, however, meet certain eligibility criteria that put them in the target group, such as being of certain age for the social pension or being out of work to receive unemployment benefit.

Table 2 Unconditional social assistance programmes

(For social pensions: see table 3)

| Latin America | |||||

| Brazil |

|

||||

| Chile |

|

||||

| Mexico |

|

Table 3 Unconditional social assistance programmes (social pensions)

| Latin America | ||||

| Argentina |

|

1948 | ||

| Belize |

|

|||

| Bolivia |

|

2008 | ||

For those who cannot work temporarily or permanently due to life contingencies, receiving unconditional social assistance can make an important difference, as it may be their only source of income. Social pensions can also make a difference. Barrientos found that social pension schemes in Brazil and South Africa have ‘a significant impact on income poverty among households with older people (…).Poverty headcount would be 4.2 percent higher for the Brazil sample and 2.8 percent higher for the South Africa sample if pension income is removed and there are no off-setting changes’.12

For Brazilian subsistence farmers, the money they receive through a social assistance programme may help, but as The Economist writes, ‘[f]or someone who lives on São Paulo’s outskirts it is barely enough to cover the costs of travelling into the city centre each day in search of work’.13 According to Slater, Farrington, Holmes and Harvey, ‘[c]ash transfers are not a panacea: they may have to complement other types of transfer, and be carefully sequenced’.14

Unconditional social assistance is important because it is not dependent on work history or other conditions and treats everybody who is in need equally. But giving money to vulnerable and sometimes marginalized groups alone may not be enough for a household to move out of poverty. While income might be restored to the level of before the shock, these programmes do not invest in improving economic opportunities. They are therefore mostly protective and less promotive.

Contributory social insurance programmes

Contributory social insurance programmes provide income and assistance for work-related contingencies, events that happen during work or that influence one’s ability to work: illness, employment injury, maternity, invalidity, being fired or made redundant. Health insurance can be part of contributory social insurance as well as supplementary pensions, which differ from social pensions (which are non-contributory and unrelated to retirement).

The two types of social assistance discussed above, conditional cash transfers and unconditional social assistance, are both non-contributory: someone in need does not have to pay to receive the benefits. These programmes are paid through government revenues. Social insurance, however, is contributory. In these work-related schemes, both the employer and the employee usually pay. How much recipients have to pay for a contributory scheme can be based on their income or can be tax deductive, so that it may still be relatively affordable for the poorest people in society. The Brazilian Previdência Social Rural scheme described in box 1 is a good example of a programme for which rural, informal workers pay less than formal sector employees.

Social insurance is usually restricted to formal employment. That makes it less relevant to people in the informal sector, who account for 60% of the global workforce and the largest majority of whom are found in developing countries.15 As described in box 2, informal sector workers usually have to fall back on solidarity networks for social protection.

Contributory social insurance programmes are not directly promotive, but especially protective. The importance of being insured against a fall in income is emphasized by Ajwang: ‘a significant proportion of households that have become poor did so as a result of serious illness, which resulted in their liquidating assets to pay for healthcare services’.16 If insurance can prevent people from selling the few assets – livestock, agricultural equipment, a motorcycle – they have, spiralling into poverty is less likely.

The New Cooperative Medical Scheme in China is ‘the world’s largest rural medical insurance programme’.17 It is financed by contributions from both participants and the state. The 2010 European Report on Development concluded that health costs remain high for participants of the scheme in rural China and that it does not guarantee access to health care everywhere.18 In his blog post at The Broker, Arjan de Haan describes how this system has been developed in the history of China and concludes that although not everybody has equal access to health care, ‘its government now recognizes [that] a number of interrelated governance reforms are required’.

Instead of, or in addition to, social insurance programmes that provide access to health care, many developing countries have made their public health services free of charge. For poor people this may be the only way they can make use of these services, but usually the quality is not very high and the waiting lines are long.

Box 1 Rural Social Insurance in Brazil

Brazil has an official social protection programme targeted at rural workers, including smallholder farmers. The Previdência Social Rural (Rural Social Insurance) programme provides cash transfers to rural workers aged 55 (women) or 60 (men) and above. In 2002, the programme had 4.6 million beneficiaries.19 Formally, the programme is contributory, with a contribution based on the commercialized value of the rural products of the farmer. But rural workers who work individually or under a family economy regime (the ‘specially insured’) pay less than rural producers and salaried rural workers.20 Cash transfers are partly used to buy tools and seeds to continue working.21 The insurance includes benefits in cases of old-age, disability, accident, illness and maternity, and provides a survivor’s pension and reclusion aid.

Labour market interventions

Labour market interventions include policies, programmes and institutions to protect people against unemployment, poverty and work injuries.22 They do so in a more promotive way than other social protection schemes, setting the standard for better living and working conditions within the labour market. Examples of labour market interventions are minimum wage legislation, minimum work standards, skills training, and programmes aimed at reducing social and economic exclusion. Most countries in the world have labour market policies of some kind. Another specific type of labour market policy are job creation approaches like the public works programmes discussed here. Table 4 lists a number of examples of public works programmes.

Table 4 Selection of labour market interventions (public works programmes)

| Latin America | ||

|

||

|

In public works programmes, participants get a job for a limited period on a public works project, such as digging water tanks as part of the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) in India. These programmes are conditional: participants only get the job if they work on predetermined tasks.

Public works programmes have an impact beyond the salary that the workers get paid: by building infrastructure, they can improve opportunities for business and communication. Devereux and Solomon report that, through the Rural Maintenance Programme in Bangladesh, saving money became easier with the introduction of bank accounts for poor women.23 And the Argentine Jefes y Jefas de Hogar employment and training programme led to a decrease in unemployment among women and a fall in poverty. However, the participants appeared to make little use of training and education facilities.24 In general, although public works programmes only offer temporary employment, they can facilitate further economic activity by the participant.

Box 2 Community social protection networks

Except for Brazil, as described in box 1, in most countries informal sector workers, smallholder farmers and other self-employed persons are not covered by social insurance programmes. These are usually only provided to people employed in the formal sector. Most definitions of social protection do not take into account the protection networks that exist outside government structures. But, as Devereux and Getu demonstrate in their volume on informal and formal social protection in Africa, informal social protection networks are widespread on the continent.25 They also exist elsewhere, for example in India, which has a community labour-based health insurance, called Vimo SEWA India.

Social protection in developing countries

The coverage of the four categories of social protection that this article distinguishes – conditional cash transfers, unconditional social assistance, contributory social insurance programmes and labour market interventions – differs among developed and low and middle income developing countries. Many middle income countries provide cash to the poorest and most vulnerable, provided that schools and health centres are visited regularly.

The provision of protective contributory social insurance in low and middle income countries is still limited, but this kind of protection is important, especially among subsistence farmers and poor households that heavily depend on income from work for their daily needs. Informal workers are rarely included in the different kinds of social protection categorized. They may have to draw upon community social protection networks based on solidarity, which may increase inequality between families of formal workers with official social protection and families of informal labourers without.

Social protection programmes alone are not sufficient to address poverty, inequality and economic exclusion. Nevertheless, as recent experiences have shown, they can be one of a mix of important tools in addressing these issues. Moreover, it is increasingly recognized that social protection can bring about economic benefits, such as increased productivity, which is not only beneficial for the national economy, but also for households themselves.

Co-readers

Armando Barrientos, Professor and Research Director at the Brooks World Poverty Institute, University of Manchester, United Kingdom.

Arjan de Haan, Program Leader, for ‘Inclusive Growth’ at the International Development Research Centre, Canada.

Marleen Dekker, Senior researcher, development economist and human geographer, African Studies Centre, Leiden, the Netherlands.

Nicholas Freeland, Independent consultant and researcher in social protection, France.

Margriet Kuster, Senior Policy Advisor, Social Development Department, Directorate-General for International Cooperation at the Ministry of Foreign Affairs, the Netherlands

Rolph van der Hoeven, Professor on Employment and Development Economics at the International Institute of Social Studies, The Hague, the Netherlands.

Footnotes

- This categorization is based on a large number of other categorizations by experts and institutions, including: FAO (year unkown), Protecting Africa’s future: Livelihood-based social protection for orphans and vulnerable children (OVC) in east and southern Africa (pdf). Policy Brief, Regional Emergency Office for southern Africa; IDS (Institute of Development Studies) (2013), Promoting Inclusive Social Protection in the Post-2015 Framework. Policy Briefing, Issue 39, July 2013; Barrientos, Armando, Miguel Niño-Zarazúa and Mathilde Maitrot (2010), Social Assistance in Developing Countries Database, Version 5.0. Brooks World Poverty Institute, The University of Manchester; ILO (2010), World Social Security Report 2010/11. Providing coverage in times of crisis and beyond (pdf); Freeland, Nicholas (2007), Superfluous, Pernicious, Atrocious and Abominable? The Case Against Conditional Cash Transfers. IDS Bulletin, Volume 38 Number 3; Mkandawire, Thandika (2005), Targeting and Universalism in Poverty Reduction (pdf). Social Policy and Development Programme Paper, Number 23, December; Devereux, Stephen, Rachel Sabates-Wheeler (2007), Editorial Introduction: Debating Social Protection (pdf). IDS Bulletin Volume 38 Number 3; GSDRC (Governance, Social Development, Humanitarian Conflict) (2013), Social protection; Asian Development Bank (ADB) (2013), The Social Protection Index: Assessing Results for Asia and the Pacific; Eurostat (2011), Social protection – social benefits by function

- FAO (year unkown), Protecting Africa’s future: Livelihood-based social protection for orphans and vulnerable children (OVC) in east and southern Africa (pdf). Policy Brief, Regional Emergency Office for southern Africa; IDS (Institute of Development Studies) (2013), Promoting Inclusive Social Protection in the Post-2015 Framework. Policy Briefing, Issue 39, July 2013; Barrientos, Armando, Miguel Niño-Zarazúa and Mathilde Maitrot (2010), Social Assistance in Developing Countries Database, Version 5.0. Brooks World Poverty Institute, The University of Manchester; ILO (2010), World Social Security Report 2010/11. Providing coverage in times of crisis and beyond (pdf); Freeland, Nicholas (2007), Superfluous, Pernicious, Atrocious and Abominable? The Case Against Conditional Cash Transfers. IDS Bulletin, Volume 38 Number 3; Mkandawire, Thandika (2005), Targeting and Universalism in Poverty Reduction (pdf). Social Policy and Development Programme Paper, Number 23, December; Devereux, Stephen, Rachel Sabates-Wheeler (2007), Editorial Introduction: Debating Social Protection (pdf). IDS Bulletin Volume 38 Number 3; GSDRC (Governance, Social Development, Humanitarian Conflict) (2013), Social protection; Asian Development Bank (ADB) (2013), The Social Protection Index: Assessing Results for Asia and the Pacific; Eurostat (2011), Social protection – social benefits by function.

3. Programmes can also be semi-conditional: e.g. the Asignación Universal por Hijo (pdf) in Argentina gives 80% of the benefit as an unconditional cash transfer; the other 20% is only received after conditions are met. In the categorization in this article, however, programmes with some conditions attached are labelled as conditional cash transfer programmes. - Programmes can also be semi-conditional: e.g. the Asignación Universal por Hijo (pdf) in Argentina gives 80% of the benefit as an unconditional cash transfer; the other 20% is only received after conditions are met. In the categorization in this article, however, programmes with some conditions attached are labelled as conditional cash transfer programmes.

- Devereux, Stephen and Melese Getu (2013), Informal and Formal Social Protection Systems in Sub-Saharan Africa. OSSREA Publications.

- As he said in a speech at the International Social Security Conference in Cape Town, South Africa, in 2008.

- GSDRC (Governance, Social Development, Humanitarian Conflict) (2013), Social protection; IDS (Institute of Development Studies) (2013), Promoting Inclusive Social Protection in the Post-2015 Framework. Policy Briefing, Issue 39, July 2013; Barrientos, Armando (2008), Social transfers and growth: a review (pdf). Chronic Poverty Research Centre working paper no. 112; Reimers et al. (2006). In: Barrientos, Armando (2008), Social transfers and growth: a review (pdf). Chronic Poverty Research Centre working paper no. 112; De la Brière, Bénédicte, Laura B. Rawlings (2006), Examining Conditional Cash Transfer Programs: A Role for Increased Social Inclusion? (pdf) The World Bank Institute, SP Discussion paper no. 0603.

- De la Brière, Bénédicte, Laura B. Rawlings (2006), Examining Conditional Cash Transfer Programs: A Role for Increased Social Inclusion? (pdf). The World Bank Institute, SP Discussion paper no. 0603

- Molyneux, Maxine (2008), Conditional Cash Transfers: A ‘Pathway to Women’s Empowerment’? (pdf)

- Freeland, Nicholas (2007), Superfluous, Pernicious, Atrocious and Abominable? The Case Against Conditional Cash Transfers. IDS Bulletin, Volume 38 Number 3, p.76.

- GSDRC (Governance, Social Development, Humanitarian Conflict) (2013), Social protection

- Armando Barrientos, Miguel Niño-Zarazúa and Mathilde Maitrot categorize social assistance programmes on the basis of their contribution to development and not on whether they attach conditions. In their Social Assistance in Developing Countries Database, the authors distinguish three types of social assistance programmes: pure income transfers, income transfers plus, and integrated poverty reduction programmes. In his article in The Broker’s Social Protection Dossier, Barrientos elaborates on his method of categorization. The authors include both conditional cash transfer programmes and unconditional social assistance programmes in each of the three categories. Some of the programmes that they categorize as income transfers plus are labelled conditional cash transfer programmes by De la Brière and Rawlings (2006) (pdf). In this article, social assistance programmes are distinguished on the basis of their conditionality.

- Barrientos, Armando (2003), What is the impact of non-contributory pensions on poverty? Estimates from Brazil and South Africa (pdf) Chronic Poverty Research Centre. CPRC Working Paper No 33, p. 14

- The Economist (2013), Social spending in Brazil. The end of poverty?

- Slater, Rachel, John Farrington, Rebecca Holmes, Paul Harvey (2008), A Conceptual Framework for Understanding the Role of Cash Transfers in Social Protection (pdf). ODI Project Briefing, Overseas Development Institute, London

- OECD Development Centre (2009), Is Informal Normal? The 60-second guide

- Ajwang. In: Devereux, S., M. Getu (2013), Informal and Formal Social Protection Systems in Sub-Saharan Africa. OSSREA Publications.

- De Haan, Arjan (2013), Why Emerging Economies Need Social Policy: the Cases of China and India (pdf). International Policy Centre for Inclusive Growth (IPC – IG), One Pager

- European Report on Development (ERD) (2010), Social Protection for Inclusive Development – A new perspective in EU co-operation with Africa (pdf)

- GESS (Global Extension of Social Security) (2006), Prêvidencia Rural.

- Duarte Barbosa, Edvaldo (year unknown), Brazil. The Rural Social Insurance Programme. Volume 18: Successful Social Protection Floor Experiences, p. 81-98.

- Barrientos, Armando, Miguel Niño-Zarazúa and Mathilde Maitrot (2010), Social Assistance in Developing Countries Database, Version 5.0. Brooks World Poverty Institute, The University of Manchester.

- Not all institutions and studies include labour market interventions in their categorizations of social protection. But although they are not programmes or transfers someone can take or receive, this article considers these interventions to be part of social protection because they protect workers. GSDRC, Asian Development Bank, IDS and Barrientos also refer to labour market interventions and/or public works programmes in their conceptualizations of social protection, although Barrientos does not consider the MGNREGA a labour market intervention.

- Devereux and Solomon (2006). In: Social Transfers Evidence

- Devereux and Solomon (2006). In: Social Transfers Evidence

- Devereux, S., M. Getu (2013), Informal and Formal Social Protection Systems in Sub-Saharan Africa. OSSREA Publications.

- Muiruri. In: Devereux, S., M. Getu (2013), Informal and Formal Social Protection Systems in Sub-Saharan Africa. OSSREA Publications.

- Chirisa. In: Devereux, S., M. Getu (2013), Informal and Formal Social Protection Systems in Sub-Saharan Africa. OSSREA Publications

- ILO (2006), Social Protection and Inclusion: Experiences and Policy Issues. Geneva: International Labour Office.