The structural causes of the euro crisis – high unemployment, low growth rates and debt-ridden states in the eurozone – are not the fault of lazy Greeks, Portuguese and Spaniards. The euro itself cannot be blamed either. The problem is that the European single currency is part and parcel of an economic and financial model which contains all the ingredients for the current crisis. For example, deregulation of the financial markets went hand in hand with indebtedness of the eurozone countries. Economies within a single currency zone need to harmonize, but the national economies in the eurozone developed in very different directions, increasing the imbalances between the member states. The key to finding the right answer to the crisis is understanding the debts and imbalances in the eurozone. Just blaming debtor states like Spain, Portugal, Italy and Greece and focusing reforms on them, as is the case at present, is to ignore the whole picture. Other solutions for recovery were possible, but a deliberate policy choice was made to offload all the rebalancing efforts onto the weakest economies.

About our living analysis on the euro crisis

The first article, ‘Ideals versus reality – a false start for the Eurozone‘, looks at what has become of the ideals of the Eurozone through some reality checks.

This second article focuses on the economic analysis of sovereign debt and imbalances within the Eurozone.

Reckless debtors and reckless creditors

The German finance minister Wolfgang Schauble, backed by his counterparts in other creditor countries, is keen to say that the Southern member states of the eurozone did not invest in labour market reforms and did not build competitive sectors for the future. According to him, the blame for the financial problems in Greece lies entirely with the Greeks: ‘The reasons for Greece’s problems can be attributable only to Greece and not to actors outside the country, and certainly not in Germany.’ Although this is often the only discourse heard in the mainstream Northern European media, most economists actually take the opposite view and argue that the creditor countries, such as Germany, the Netherlands and Finland, are equally to blame. Professor Paul de Grauwe of the London School of Economics explains this most clearly. ‘For every reckless debtor there must be a reckless creditor,’ he says. In other words, you cannot blame just the countries with heavy debts for being in that situation, as their plight is the result of an interplay between debtor and creditor.

Background article

The argument that pits the lazy Greek or Spaniard against the hard-working Dutchman or Fin is clearly too simplistic. Instead of a clash of nations, we should rather speak of a clash of economic classes.

De Grauwe is certainly not alone. Cambridge economist John Ryan took a similar stance in the journal Policy Review: ‘The most striking single macro-economic feature of the Euro introduction,’ he explains, ‘was the near total convergence of risk-free government bond rates among the Eurozone members.’ In other words, credits from countries with a current account surplus, mainly Northern European countries, began to flow into the financial system of countries in the South as interest rates across the eurozone were plummeting. The creation of the single currency convinced the financial sector that government borrowing was now a very safe investment across the eurozone, because countries were no longer able to nominally devalue. As a result, for many governments, including those of Greece, Spain and Italy, the costs of borrowing fell to historically low levels.

Esteban Pérez-Caldentey & Matías Vernengo – The Euro Imbalances and Financial Deregulation: A Post-Keynesian Interpretation of the European Debt Crisis ‘Conventional wisdom suggests that the European debt crisis … was caused by fiscal profligacy on the part of peripheral, or noncore, countries in combination with a welfare state model, and that the role of the common currency – the euro – was at best minimal… contrary to conventional wisdom, the crisis in Europe is the result of an imbalance between core and noncore countries that is inherent in the euro economic model. Underpinned by a process of monetary unification and financial deregulation, core Eurozone countries pursued export-led growth policies – or, more specifically, “beggar thy neighbour” policies – at the expense of mounting disequilibria and debt accumulation in the periphery.’ Jörg Bibow – The Euro Debt Crisis and Germany’s Euro Trilemma ‘…key institutions and policies have failed in securing the convergence and cohesion required for EMU member countries’. ‘Intra-area competitiveness and current account imbalances, and the corresponding debt flows that such imbalances give rise to, are at the heart of the matter, and they ultimately go back to competitive wage deflation on Germany’s part since the late 1990s. Germany broke the golden rule of a monetary union: commitment to a common inflation rate.’ Paul De Grauwe – The Financial Crisis and the Future of the Eurozone ‘…the method of convergence implicit in the SGP has not worked well – macroeconomic divergences have stubbornly remained for nearly a decade and several countries experienced boom and bust dynamics. Although strong declines in real interest rates may explain part of the story (but e.g. Italy did not experience boom & bust), self-fulfilling waves of optimism and pessimism which might be called ‘animal spirits’ and are of mainly national origin, seem a good candidate for explanation. These national animal spirits endogenously trigger credit expansion and contraction. It follows that (national) movements of credit ought to be under much firmer control and this is up to the monetary authorities, including the ECB.’Some sources about the imbalances in the eurozone

Lending to eurozone governments and banks became very attractive and was further stimulated by reforms in the Basel II banking regulatory framework. The deregulation of financial markets coupled with the introduction of the single currency made if very profitable for the financial sector to loan money to Southern European countries. The capital flowing out of Germany, the Netherlands and other countries with a current account surplus and on the lookout for safe investments began to be loaned across the eurozone in large quantities to governments, companies and individuals. The result was cheap capital flowing into Spain, Portugal, Italy and Greece.

Around the time the euro was being established the EU also deliberately engineered changes to the global Basil II regulatory framework so that European government borrowing was categorized as risk free and eurozone interbank lending was categorized as being almost risk free, as can be read in a KPMG report from 2003. Now European banks could lend to other governments or other eurozone banks without keeping capital in reserve as insurance against defaults.Basil II regulatory framework

These massive credit flows led to escalating private and business debt in Southern Europe. Consumption levels rose and the booming demand for labour drove up wages, especially in Spain, Ireland and Greece. These receiving countries all enjoyed much higher growth rates than Germany and the Netherlands in the years leading up to the crash of 2007 and their economic growth and escalating house prices made it more attractive to invest in these countries. Rising wages increased the demand for imported products and inflated local prices. This made cheaper Northern European imports even more attractive, increasing the trade surplus even further in Germany and the Netherlands. And so the imbalances grew ever bigger, fuelling further lending and debt-financed spending. In Ireland and Spain in particular, speculative property bubbles began to inflate, and in Greece and Italy government debt ballooned. All this was fuelled by cheap capital flowing out of surplus countries such as Germany, the Netherlands and Finland.

According to OECD data, average annual wages in Greece increased by 52.0% between 2000 and 2010. In Spain the wages increased by 42.6% and in Ireland by 53.2%. The lowest increase was in Germany, with a 16.7% increase in the average annual wage between 2000 and 2010. In most other eurozone countries wage increases were somewhere between these two extremes: Netherlands 34.0%, France 32.7%, Belgium 25.5% and Luxembourg 34.6%, for example. After 2010 wages continued to increase, with the exception of Portugal and Greece where wages decreased. In Spain and Italy wages stayed the same from 2010 to 2014. Bloomberg took a look at statistics from the Bank for International Settlements and worked out that German banks loaned out a staggering $704 billion to Greece, Ireland, Italy, Portugal and Spain before December 2009. According to numbers compiled by BusinessInsider, two of Germany’s largest private banks, Commerzbank and Deutsche Bank, loaned $201 billion to Greece, Ireland, Italy, Portugal and Spain. For a nice overview of debts between European states, the BBC also published this insightful graph: Who owes what to whom?Wage and debt increase in Southern Europe

Source: McKinsey Global Institute report 2012.

Why was this capital not invested wisely, for example to improve productivity and competitiveness in the global market? Why did governments not interfere? To answer that question, we can turn to the work of economist Michael Pettis. His work demonstrates that there is no example in history of governments being able to handle such large capital inflows in a proper and coordinated way. They are simply overwhelmed by the massive capital influx from creditor countries. Sensible investments fall by the wayside in favour of short-term prestige projects based on optimistic speculation.

‘From 1871 to 1873 huge amounts of capital flowed from France to Germany. The inflow of course drove the obverse current account deficits for Germany, and Germany’s manufacturing sector struggled somewhat as an increasing share of rising domestic demand was supplied by French, British and American manufacturers. But there was a lot more to it than mild unpleasantness for the tradable goods sector. The overall impact in Germany was very negative. In fact economists have long argued that the German economy was badly affected by the indemnity payment both because of its impact on the terms of trade, which undermined German’s manufacturing industry, and its role in setting off the speculative stock market bubble of 1871-73, which among other things unleashed an unproductive investment boom and a surge in debt. ‘As Germany began to absorb the inflows, its current account surplus of course reversed into deficits, which by definition means that there was a large and growing excess of investment over savings. Part of this was caused by rising German consumption, but much of it was caused by surging investment….As money poured into Germany the German economy boomed, along with German consumption, investment (a growing share of which went into projects at home and abroad that turned out in retrospect to be overly optimistic), and into the Berlin and Viennese stock markets. By early 1873 more experienced German, Austrian and British bankers were quietly warning each other of a speculative mania, and they were right. The stock market frenzy culminated in the 1873 global stock market crisis, which began in Vienna in May, shortly after the beginning of the 1873 World Fair, and rapidly spread throughout a world brimming with liquidity (a large part of the first French indemnity payments went directly to London to pay outstanding German obligations). By September the crisis reached the United States with the collapse of Jay Cooke and Company, one of the leading US private banks, and for the first time in history the New York Stock Exchange was forced to close, for ten days. The subsequent global “Long Depression”, which lasted until 1896, was felt especially severely in Germany, one of whose first reactions was the collapse of the railway empire of Bethel Henry Strousberg, a major industrialist at the time… ‘Within a few years of the beginning of the crisis attitudes towards the French indemnity had shifted dramatically, with economists and politicians throughout Germany and the world blaming it for the country’s economic collapse. In fact so badly was Germany affected by the indemnity inflows that it was widely believed at the time, especially in France, that Berlin was seriously contemplating their full return. The great beneficiary of French “largesse” turned out not to have benefitted any more than Spain had benefitted from German largesse 135 years later. This is interesting. The German economy responded to French capital inflows in almost the same way that several peripheral European economies responded to large German capital inflows 135 years later….It might seem an unfair comparison at first because the 1871-73 transfer to Germany was huge, but it turns out that the magnitude of the French transfer into Germany was broadly similar, in fact probably smaller, to the inflows into peripheral Europe….Spain’s debt and its fiscal accounts were far stronger than the European average and stronger than those of Germany in most respects.’From Michael Pettis’s blog

In addition to this paralysis of government common sense, the increasing role and influence of the financial sector in the economy, called ‘financialization’, favours short-term profit over longer term performance, making it even harder to invest money in creditor countries for the purpose of securing economic stability. It simply became easier to make short-term profits from investments in Southern Europe and many creditor countries found themselves investing less at home and more abroad. These low investment rates at home resulted in lower productivity levels, which had to be compensated by lowering wages, in turn raising the short-term competitiveness of Northern European countries. The competitiveness of the Southern eurozone countries suffered in the longer run.

The myth of export-led growth

So, can we hold the euro responsible for the crisis, especially as the differences in international competitiveness already existed before it was introduced? Well, we can hold it partly responsible. Countries like Germany, Finland and the Netherlands benefited from the introduction of the single currency and increased their export base because the value of the euro was far too low for their economies; the value of their own currencies would have been much higher. At the same time, the value of the euro was too high for the economies of Spain, Portugal, Greece and Italy; the value of their own currencies would have been lower than the current value of the euro.

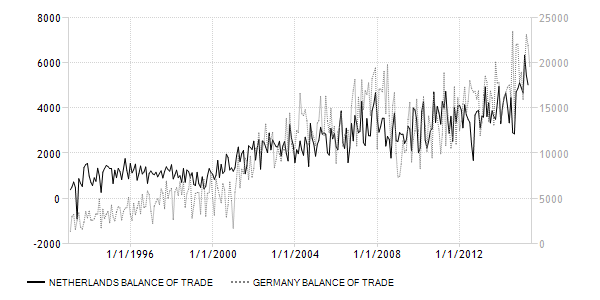

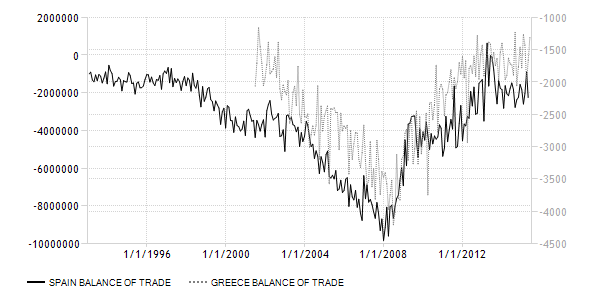

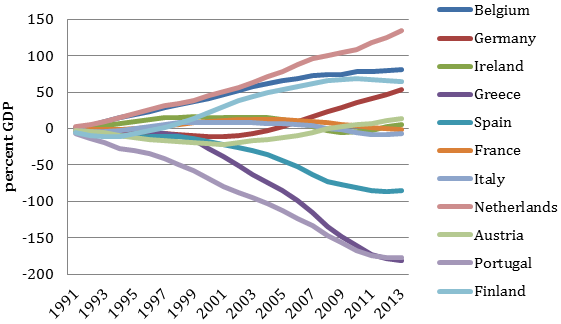

The Dutch and German trade surpluses increased rapidly after 2000, despite low productivity growth. These surpluses were created by the undervaluation of their export products in combination with wage moderation and labour market reforms to increase competitiveness. Figure 1 shows the monthly trade balance of both countries measured in million Euro. Monthly trade balance for Germany and the Netherlands in million Euro (source: www.tradingeconomics.com) The increase in their current account surpluses has been spectacular. In the Netherlands the current account rose to more than 10% of GDP in 2013 and 2014. The German current account surplus has been above 6% of GDP since 2008 and increased to nearly 8% in 2015. Both countries are therefore significant lenders to other countries that have a negative current account. The opposite can be seen in Italy, Spain and Greece. After 2000 their trade deficits increased significantly until 2008. By 2007, Spain had the second largest trade deficit in the world (behind the US) in absolute terms at nearly 10 billion euros on a monthly basis. Monthly trade balance for Spain and Greece in thousand euro (source: www.tradingeconomics.com) The trade balances of Spain, Portugal, Italy and Greece have improved since 2008, but there are different explanations for these. In Greece the rebalancing of the trade deficit is purely the result of a decline in imports due to a fall in domestic demand rather than a rise in exports. In Spain, Portugal and Italy the improvement was due to both a decline in imports and some increase in exports. These countries were able to increase their exports within the midst of the economic crisis for two reasons. First, the decline in the value of the euro against the dollar and pound after 2008 made exports cheaper in non-euro countries. In particular, the drop in labour costs (in Spain 13% in comparison with Germany since 2009), and especially lower wages, due to the policy of ‘internal devaluation’ in the eurozone has increased some exports and started a race to the bottom on labour costs to improve competitiveness. Current account of the main eurozone economies (expressed as a percentage of GDP). Source: Simon Taylor (2011), Fallacies of Composition Figure. Cumulative current account as a percentage of GDP starting in 1991 for eurozone countries (source: European Commission, Ameco / Used from Paul De Grauwe’s article Secular Stagnation in the Eurozone)Imbalances – winners and losers of the single currency

In other words, Northern countries in the eurozone were able to significantly improve their competitiveness because of the undervaluation of the euro in relation to their economic performance, in combination with a policy of wage moderation. This came at the cost of the Southern countries. Without the euro, exchange rate differences between the eurozone countries would make Spain, Italy, Greece and Portugal more competitive on the international market, while German, Finnish and Dutch exports would be more expensive, resulting in higher unemployment and lower economic growth in these countries.

To quote John Ryan, who is economist at the University of Cambridge: ‘Germany’s economic success is a product of a combination of nominal wage restraint, supported by labour market reforms that have put downward pressure on wages, and severe spending restraints on public investment as well as on research and development and education.…Finally, weak spending on public infrastructure lowers the potential for productivity increases at home.’ For Germany the worst costs has been the lack of productivity growth, with current productivity level more or less the same as ten years ago. And because a lack of productivity growth means low wage growth, real wages in Germany stagnated for up to two decades. And it shows that the German economic growth was mainly due to its increase of current account, stimulated by the undervaluation of the Euro for German’s economic activities and low wages, and not due to its productivity or increase in domestic demand.Germany's economic success

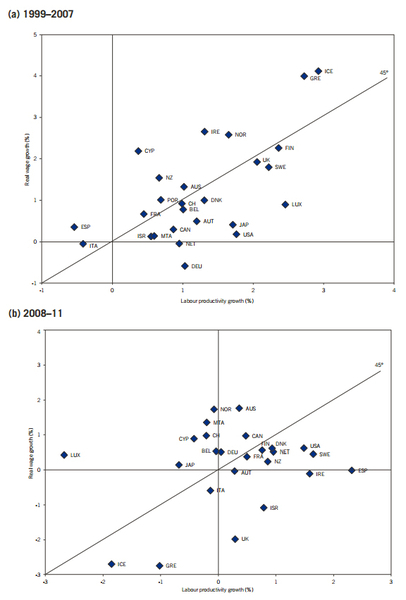

Growth in real wages and labour productivity in developed economies,

1999–2007 and 2008–11 (%). Source

The global financial crisis of 2008 halted the flow of capital into Southern European member states. The property bubbles in Spain and Ireland burst and many banks with huge stakes in the property business instantly became insolvent as the value of their assets plummeted. As the property market crashes in Ireland and Spain threatened the banking systems in those countries with collapse, the Irish and Spanish governments bailed out their banks, leaving them with a mountain of public debt.

The end of cheap capital flows and greater uncertainty in the financial markets began to force up the costs of refinancing government debt in Southern European countries. The previously harmonizing interest rates split apart and for some governments the cost of borrowing became more expensive. Some countries, such as Greece and Italy, found themselves paying huge rates of interest to roll over their loans and as a result their debt mountains began to grow uncontrollably. The European Central Bank, other EU governments and the IMF loaned money to Southern European countries, but 90% of that money was given to banks to pay off their bad loans to prevent widespread banking collapses across the eurozone, turning yet more private debt into public debt.

One response to this could have been to rebalance the eurozone. Although surplus countries cannot revalue their currencies to rebalance their trade relationships with the rest of the eurozone, they could achieve the same effect by allowing domestic costs to inflate, for example by increasing wages. In October 2013, the US Treasury Department’s currency report noted: ‘Within the euro area, countries with large and persistent surpluses need to take action to boost domestic demand growth and shrink their surpluses.…Stronger domestic demand growth in surplus European economies, particularly in Germany, would help to facilitate a durable rebalancing of imbalances in the euro area.’ And in 2012 Bundesbank chief economist Jens Ulbrich also openly supported a significant rise in wages as part of a recovery strategy. Wages did rise a little and Germany introduced a minimum wage, but these measures were limited.

Bundesbank Chief Economist Jens Ulbrich told Der Speigel that recently agreed pay rises of more than 3% were welcome and that recent wage trends were ‘moderate’ given Germany’s relative economic strength and low unemployment. Germany’s average worker’s wage has hardly risen over the last decade, as in the UK and USA.Minimum wage Germany

Instead, the EU position on solving the euro crisis was to concentrate purely on the debtor countries. It asserted that recovery was only possible by cutting public spending (austerity), reducing wages and social costs (internal devaluation), and running a trade surplus (export-led growth). As Simon Wren-Lewis, professor of economics at Oxford University, said, ‘wages and prices are “sticky”, this adjustment will not happen quickly’. The price of such measures is high, including long-term high unemployment and low wages.

The idea behind this recovery package is that rising competitiveness will boost exports and growth, generating income to pay off the debts. In 2010 the European Commission opted for liberalizing collective bargaining and introducing structural supply-side reforms of the labour market. In 2011 a new report assumed, again, that a loss of competitiveness was the main problem and an export-led growth model should be implemented, along with measures for national governments to cut public spending and impose supply-side reforms in the labour market. In other words, the strategy of the eurozone is to strive for every country to be like Germany or the Netherlands or Finland.

European Commission, ‘Excessive Imbalance Procedure’, 2011. It led to EU regulations 1174 and 1176 under which the European Union monitors the economic developments of member states. A mechanism was introduced to prevent and correct excessive macroeconomic imbalances, backed by sanctions if a eurozone member state repeatedly fails to comply with the recommendations made at European level. Excessive Imbalance Procedure

The reality is that slashing domestic demand in economies that are not export-driven will hardly increase growth rates in the short term, which is needed to create jobs and pay back the creditors, and that transforming these countries into export-led economies is a long-term strategy. To become an export-led economy needs time and above all intensive investments. ‘If European policymakers are serious about enhancing the competitiveness of these countries it will require huge levels of social investment in education, training and research, not to mention institutional capacity building. All of this expenditure implies that member states should ignore the political and legal treaties of the European Union,’ writes Aidan Regan of the Max Planck Institute for the Study of Societies.

‘In the Eurozone, one can argue that there are two variants of capitalism. Northern European countries; Germany, Austria, Netherlands and Finland are often described as coordinated market economies (CMEs). They have centralized and economically sophisticated employers and trade union associations with the capacity to autonomously coordinate and solve complex labour market problems. In addition, they have embedded welfare state traditions committed to social protection and income security. They have traditionally relied upon export-led growth as a mechanism to generate employment. Hence their macroeconomic structure supports a preference for stable fiscal policies and supply-side labour market reforms.’ ‘One the other hand, southern European countries in the Eurozone; Spain, Italy, Cyprus Greece and Portugal, are often described as mixed-market or Mediterranean varieties of capitalism. They have fragmented trade unions and employers with limited capacity to coordinate labour market outcomes. They have weak welfare states and a significant amount of social security occurs through family relations. Traditionally, they have generated economic and employment growth through domestic consumption. This gives priority to domestic demand over export-profits. Prior to EMU this structure lent itself to an accommodating monetary and fiscal policy, with governments regularly devaluing the currency to offset a loss of competitiveness and the inflationary impact of domestic prices.’ Source: Aidan Regan, ‘One size fits all approach risks intensifying Europe’s North South divide’, Max Planck Institute for the Study of Societies, Cologne, Germany Two varieties of capitalism

Besides, it is economically impossible for all eurozone countries to become like the Netherlands and Germany. All trade surpluses have to be matched by trade deficits elsewhere, so the idea that everyone can have a simultaneous trade surplus is impossible. This echoes the argument by Financial Times columnist Wolfgang Munchau that ‘the failure [of the eurozone] to adjust to the necessities of a large closed economy is the single largest force behind the crisis’. A significant trade surplus for the whole eurozone, even if it were possible, would imbalance the world economy even further and ultimately have a negative impact on Europe as well. And which deficit countries would they export to?

Economist Simon Taylor: ‘German and other experts on the euro crisis have been guilty of a fallacy of composition. This means falsely assuming that what is true of the parts is true for the whole. Concretely, since the eurozone is more or less a closed economy (it has a roughly zero balance of payments with respect to the rest of the world, which is not the same thing but is near enough for this purpose) policy measures which are rational for individual open economies are potentially disastrous for the whole zone.’ It is possible in principle for the whole eurozone to run a significant surplus with respect to the rest of the world economy, but as economist Simon Taylor explains, as one of the three largest economies in the world, it would exert downward pressure on global GDP and be very unwelcome to both the US and China, the other two large economies in the world. Therefore, the strategy of trying to make all EU countries like Germany or the Netherlands is ‘both unhelpful and to some extent rather stupid… Either the German politicians understand this and are therefore dishonest or they don’t in which case they are criminally ignorant. I’m not sure which is the case.’ In economic terms, more solidarity between the eurozone countries in which the countries that lose out in the eurozone could to a certain extent be compensated by the winners is not such a strange option for long-term stability within Europe and for the rest of the world as well, while allowing countries to pursue their own economic path. Simon Taylor explains

The rise of the debt state

We know now that imbalances in the eurozone between surplus and deficit countries have triggered a capital flow of cheap debts to the Southern European countries in particular. But this does not explain why it has run out of control. That can only be explained by the deregulations in the financial sector. What happened at the national level is the same as what happened to countless households. Before the financial crisis low-income families received a lot of cheap credit and they are now struggling to pay off their debts.

Read here some expert opinions on the impact of the financial sector on the functioning of the economy: Dean Baker, co-director of the Center for Economics and Policy Research in Washington DC, writes about the impact on growth of a financial sector that is too large: “[T]here is evidence that a bloated financial sector is a major impediment to growth. While advanced economies need a well working financial sector to allocate capital from savers to those who want to borrow, when the sector gets too large relative to the size of the economy, it is simply a drag on growth. From this vantage point, policies designed to reduce the size of the sector, such as a financial transactions tax, will help to boost growth while at the same time hitting some of the highest earners in the economy”. Stewart Lansley, a visiting fellow at Bristol University and the author of The Cost of Inequality, Gibson Square, explains in his expert opinion how high profits increase inequality: “The overwhelming evidence is that, contrary to the pre-2008 market theory, excessive levels of inequality slows growth and makes economies much more prone to crisis. The great surge in inequality from the 1980s not only blew us over the cliff in 2008, it also prolonged and deepened the downturn, and is now sowing the seeds for the next meltdown. The surge in inequality over the last three decades has been driven by a great shift in the share of the economic cakes colonized by capital rather than labour. The sustained shift from wages to profits has been a seismic economic change described by the Geneva-based International Labour Organization as creating a ‘dangerous gap between profits and people’. It is a process that continued through the crisis. While living standards have been falling, corporate profitability has reached new heights. The world is awash with spare capital – a mix of corporate surpluses and privately-owned liquid wealth. According to market theory, the rising profit share should have led to an economic leap forward. Instead, shrinking wage pools have depressed demand, while the surpluses created have been spent in ways that have destabilized economies, distorting incentives and fueling a boom in financial engineering that has enriched the few while undermining the productive economy. Investment banks are already promoting a new version of the lucrative collateralized debt obligation, the financial product that wreaked so much havoc in the build-up to 2008.” Ken-Hou Lin, Assistant Professor of Sociology at the University of Texas at Austin, writes about the stagnation of labour demand in the US due to financialization: “My ongoing study of the largest US corporations indicates that the stagnation in labour demand is linked to the rise of finance through three pathways…When comparing non-financial companies that engage in financial activities with those who focus on their core business, I find that the former tend to have much weaker employment growth than the latter. Second, as discussed in Eileen Appelbaum’s opinion article [See below], my study shows that system-wide excessive leveraging is detrimental to long-term job growth. Compared to companies primarily funded by equity, debt-loaded companies are under constant pressure to meet fixed obligations. As a result, these companies face greater layoffs during recessions and are more conservative in expanding their workforce even during economic booms…My analysis shows that companies that are more generous in terms of dividend payment and stock repurchase tend to have weaker job growth. More importantly, the tradeoff relation has been increasing over time, suggesting that executives today are less reluctant to reward shareholders at the expense of employment.” Eileen Appelbaum, Senior Economist at the Center for Economic and Policy Research in Washington DC and Visiting Professor in the Department of Management at the University of Leicester in the UK, writes about debt ridden companies due to investment banks and private equity: “One of the lessons of the financial crisis of 2008 is that the excessive use of debt undermines the stability of the financial system and poses a threat to companies and their workers…Policy makers in the US and elsewhere should take steps to discourage the risky use of debt. Here are three ideas: 1) Limiting the tax deductibility of interest would make over-leveraging companies less attractive. 2) Financial institutions could be required to limit loans so that a substantial part of the debt can be repaid over a five-year period. 3) The limited US regulatory oversight of private equity firms could be expanded along European lines so regulators can assess how risky the debt leveraged on companies is and impose limits if necessary. This last proposal is already implemented in the European Commission’s Alternative Investment Financial Managers Directive (AIFMD). Policies that limit leverage to limit risk are long overdue.”Related expert opinions from The Broker

Money found its way to these countries and households in such large quantities because of a shift in the economy from labour towards capital. Less money was invested in productive sectors to increase productivity and improve labour and more was put into short-term speculative ventures. As economist Rolph van der Hoeven wrote in an article for The Broker, ‘Financial globalization has especially weakened workers’ bargaining positions as capital is much more mobile and can move more easily to other regions.’ Moreover, in the drive to maximize shareholder value, labour is seen primarily as a cost, which explains the policy of cutting wages rather than investing in higher productivity. (See more on the shift from labour to capital in the background article.) Because this took place in the mid-1990s when many governments were busy reducing their budget deficits by cutting back on the welfare state, the demand side of the economy slumped. The gap was filled by cheap credits, which drove many low-income families into very lucrative debt contracts for bankers.

Background article

Profits are reinvested less in productive sectors, where labour can benefit, and more in capital markets.

One logical but simplistic conclusion could be that the euro crisis was caused by bad or greedy investors, bankers and corporate managers. But this ignores the fact that they changed their practices and business models after policy changes allowed them to do so. These policy changes deregulated the financial market, put the shareholder economy above a stakeholder economy and de-standardized labour contracts. The financial market was indeed very willing to adapt quickly to this new situation of self-regulation, but it is complex and its actors are not aware – and not encouraged to be aware – of their actions in the broader societal context, creating huge risks of financial booms and busts. According to Cambridge economist Ha-Joon Chang, neoliberal market economies are more often prone to financial bubbles than in the era before the 1980s, when markets were more regulated. He demonstrates this by pointing to the Asia crisis in 1998, the dot-com bubble of 2000, the financial crisis in Argentina in 2001, and the global financial crisis in 2008.

As journalist Koen Haegens argues in his book The biggest show on earth, the myth of the market economy, there is no such thing as a ‘market economy’, a set of markets that functions to establish efficiency in the economic system. ‘In the property market and in the financial sector, bubbles have been created. Those bubbles suddenly busted. How does that rhyme with the idea that markets, at least on the long term, will generate stabile equilibrium between demand and supply?’ The biggest show on earth

Emeritus Director at the Max Planck Institute Wolfgang Streeck shows how financial bubbles can be linked to financialization and ultimately with the indebtedness of states. Financialization made it easier for governments to manage their debt level. The financial sector ‘soon began luring governments into substituting credit for taxes as the latter became more difficult to collect,’ he writes. The result: governments and the financial sector became very much intertwined.

According to Emeritus Director at the Max Planck Institute for the Study of Societies, Wolfgang Streeck in his paper The rise of the European consolidation state (2015), it was not redistributive policies that could be blamed for higher public debts, as this period coincided with ‘a general, equally secular decline in the political power of organized labor and social-democratic politics, as indicated by long-term sinking rates of unionization, falling participation in national elections, an almost complete disappearance of strikes, high and steady rates of unemployment, stagnant wages and rising economic inequality.’The rise of the European consolidation state

And this not only had consequences for the state. As we have seen, the banks kept demand going while public spending was being cut by providing cheap debts for households, for example to buy houses or holidays. In economics this is called ‘privatized Keynesianism’. It helped European states to stabilize their debt levels during the mid and late 1990s in comparison with the two previous decades. But, in economic terms, debts never go away; they shift from the private to the public sector. So when governments reduced their debt levels in the 1990s, it was the private sector that became overwhelmingly indebted, especially the lowest income groups, and this triggered the financial crisis.

Governments thought financialization was the solution for managing their debts levels. What happened when the bubble burst in 2008 was that banks held an array of ‘bad debts’ and it was a political choice to bail them out at the taxpayers’ cost, which ultimately led to a surge in state debt. This affected all members of the eurozone, but particularly the Southern member states because of the cheap credits they had obtained over the years due to the imbalances in the eurozone.

Systemic change

To conclude, it is not the single currency itself that can be blamed for the economic woes of our time. The picture is more complicated. The euro is part and parcel of an economic and financial model which contains all the ingredients for the current crisis. The structural causes of the economic crisis in Europe are linked to the policy choices made in the single market in the wake of the single currency, mainly related to financialization. Finding a solution is therefore not a question of simply restoring business as usual.

Financial globalization and the rise of short-term speculation did not start with the euro. The euro is a product of a long-term economic strategy that started with the single market and promotes an export model that undervalues the demand side of the economy. The answer cannot simply be to cancel the single currency and keep the single market, as this will not solve some of the root causes of the euro crisis. Abandoning the euro will not change much and arguably will be a step too far for countries like Germany, Finland and the Netherlands, as they benefit from having a global reserve currency that is undervalued in relation to their economies. They would do everything to avoid such a move because their economies are increasingly dependent on exports. Even a eurozone without Greece, Spain, Portugal and Italy would not be their preferred option, because without these countries the value of the euro would rise significantly, damaging their export potential.

Engineering a recovery while keeping the single currency needs a radically different perspective on the economy and policies taken at the supranational and national level. For example, the view that the euro can only exist in combination with a one-size-fits-all export-led economic model based on wage moderation must be disputed. New policies can only be made in a more democratic environment in which all European citizens believe they have a say in the future of the European Union. There are several alternatives to counter the political choice of returning to business as usual, bailing out the banks, shoring up faith in financial markets and encouraging more stringent wage moderation and public spending cuts. These alternatives seek to put new values into the economy and they will be discussed in Part 3 of this living analysis.

The economic model of the creditor countries has created a low-wage economy, which is not the solution for a sustainable development path either. Ángel Ubide from the Peterson Institute for International Economics wrote in the Spanish newspaper El Pais: ‘The German attitude to minimize the potential cost of monetary union is similar to the current debate about inequality – the obsession with fiscal austerity and inflation risks is explained by the focus of the better off to protect their interests as savers and investors, even if that leads to an increase in the gap between the rich and the poor.’

Any alternative approach must therefore focus on democracy, wage-led economic growth models, and countering the trend of financialization. This is only possible if citizens and politicians accept that within the eurozone there must be more solidarity – in the same way that the western part of the Netherlands subsidizes the north-eastern part of the country. The reunification of Germany was only successful because the solidarity shown by rich West Germany to poor East Germany. In the end everyone benefits, because you can only improve your welfare if your neighbours are doing well too.